Developing a business plan on specific for an insurance agency can be a relatively straightforward process although there are some complex issues that need to be addressed. Whenever we develop an insurance agency business plan, we focus on the two primary revenue streams that are produced by these entities. With equal importance, we focus on the initial sale of an insurance policy that produces a substantial amount of commission driven income. This is complemented by a discussion regarding the recurring fees of revenue that are produced from ongoing renewals. One of the key focuses of the business plan is to discuss the ongoing renewals given at this creates a highly passive stream of income that can cover a significant portion of the underlying operating cost of the agency in the coming years. The approach that we take when developing these types of documents is slightly different whether or not the insurance agency is affiliated with a major carrier or is operating in an independent brokerage capacity. In the event that the plan is specific for a carrier then we create several sections of the busniess plan that address human resources issues especially as it relates to recruitment, retention, promotion, and management.

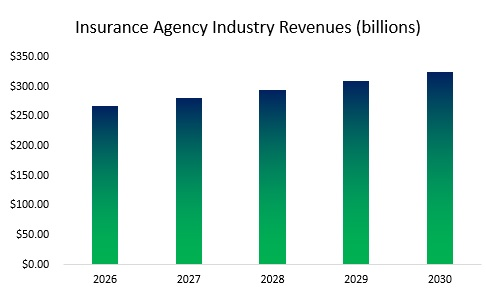

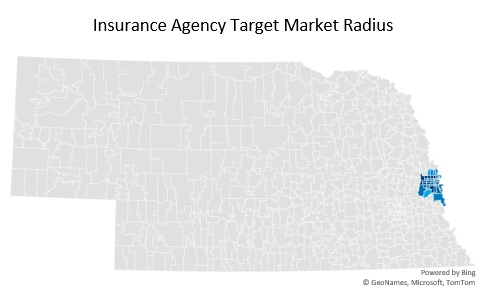

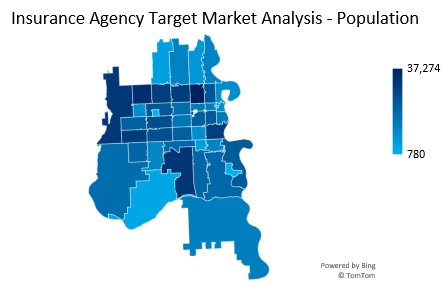

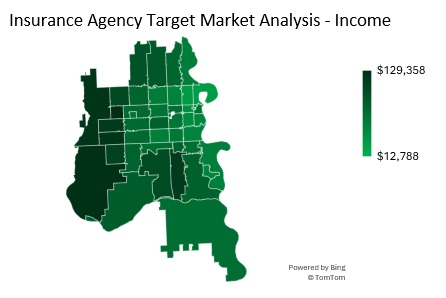

We are market research for first and we take this approach when developing a business plan specific for any insurance agency or insurance broker. Initially, we do a deep analysis of the target market area, including a demographic study regarding both individuals as well as businesses. Most insurance agencies are able to provide both personal lines as well as commercial lines. Once we determine the target market size, we then take a look at metrics relating to household income, median home value, the unemployment rate of the target market, as well as other metrics specific for the area. This allows us to gauge the economic stability of the market, which we discussed very thoroughly throughout the course of the business plan. This section of the business plan also discusses the insurance industry as a whole as well as relevant trends that may impact the operations of agencies/brokerages moving forward. This includes a review of any policy driven changes that may change the way that these businesses conduct business. Recently, we have begun to document the use of new technologies that focus on automation of the underwriting and sales funnel process.

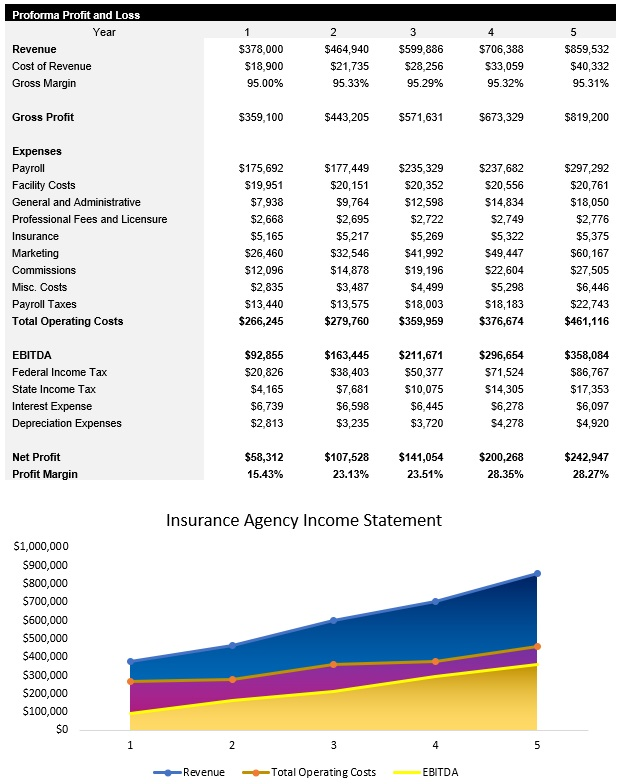

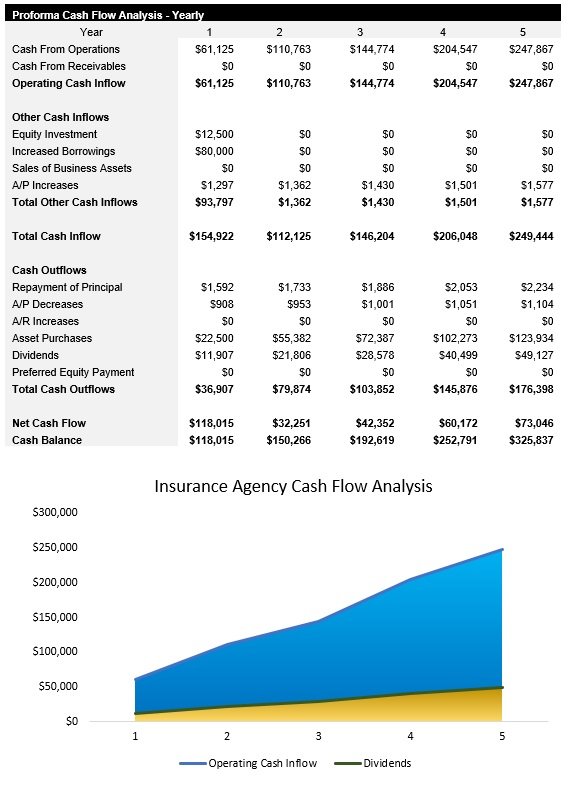

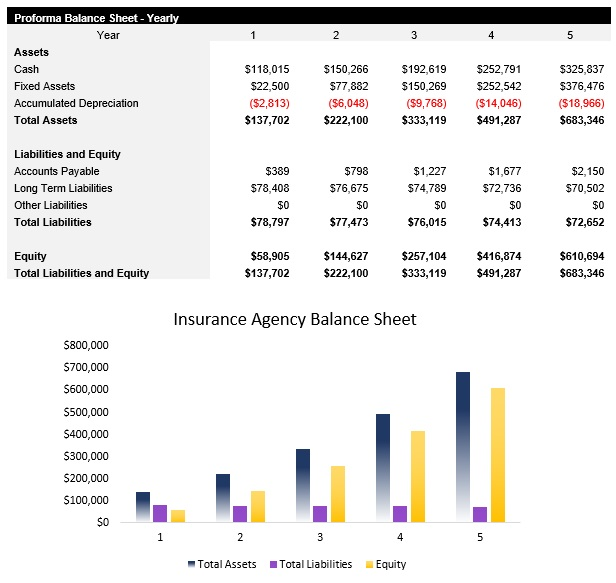

Once we have obtained and reviewed the metrics specific for the target market area. We then begin developing the financial plan. The scope of the financial model includes a five-year profit and loss statement, cash analysis, common size income, balance sheet, breakeven analysis, and specific business ratios regarding the insurance industry. If this business plan is to be presented to a carrier, we also discussed the number of policies that are produced on a monthly basis as well as production quotas.

From here, within developed the insurance agency marketing plan. Specific for these types of businesses, this is one of the more important chapters of the document. We focus very heavily on establishing ongoing referral relationships with attorneys as well as accountants in the market area. This is complemented by direct outreach with realtors that can provide referrals to people that have recently purchased or rented a home. If the insurance agency is affiliated with a carrier, then we typically put less of a focus on matters related to search engine optimization and online marketing strategies, as this is typically provided by the underwriter. In the event that this is specific for an independent broker, then we do focus very heavily on this type of marketing in order to create a significant amount of online visibility. A significant component of this discussion revolves around regional search engine optimization as this is an incredibly important part of an independent insurance brokerage’s marketing plan.

The fourth phase of this process then is the operation section of the business plan. Here, we discuss the specific types of personal and commercial lines that will be offered. We also discuss matters related to human resources and providing the necessary incentives in order to have insurance agents directly conduct outreach to secure policies on behalf of the firm.

Then we reached the conclusion, which ironically is the first chapter of the business plan. Although it may seem counterintuitive, we always developed the executive summary last as it provides a deep insight into the business, especially if this business plan is geared towards a commercial underwriter. In this section we focus on the experience of the founder, an overview of how the business will be financed, a snapshot of the anticipated financial results, as well as a discussion regarding the liability of the target market.